On June 13, at the 2025 SMM (13th) Minor Metal Industry Conference - Rare and Scattered Metal Forum (Indium, Germanium, Gallium, Bismuth, Selenium, Tellurium), hosted by Shandong Humon Smelting Co., Ltd. and SMM Information & Technology Co., Ltd. (SMM), Long Wensheng, General Manager of Changsha Aochang Nonferrous Metals Co., Ltd., delivered a speech on "The Current Application Status and Future Outlook of Minor Metal Selenium."

Selenium Industry Overview

Selenium Industry Overview: Application Areas of Selenium

Introduction to the Selenium Industry: Selenium is widely used in industries such as industry, agriculture, biomedicine, and the general health sector.

Selenium (Selenium) is a dark gray to steel gray solid with a metallic luster. Its elemental symbol is Se, and its atomic number is 34. Selenium exhibits certain metallic properties, such as electrical conductivity, and is therefore also considered a semimetal. Selenium has a density of approximately 4.81 g/cm³, a melting point of 217°C to 221°C, and a boiling point of 685°C. Its applications span multiple fields, including health and medicine, agriculture and food, industry and high technology, and environmental protection, making it an important element with broad application prospects.

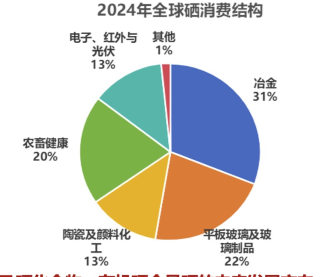

In 2024, the total global selenium consumption was approximately 3,690 mt. In terms of consumption by sector, the global selenium consumption structure was still evolving in 2024. The proportion of metallurgical consumption increased from 26% to 31%; the consumption proportion in the flat glass and glass products sector decreased by 5 percentage points to 22%; and the ceramic and pigment chemical sectors accounted for 13%.

♦Selenium Industry Trends: High-end products such as organic selenium are growth points for future market development

In the future, selenium will transition from traditional low-end markets to high-end markets, with increased demand for high-end products and the gradual phase-out of low-end products. High-purity selenium and selenium compounds, as well as organic selenium, will be the future development directions for selenium. Domestic and overseas applications of organic selenium are mainly in agriculture, forestry, animal husbandry, human health care, and medicine. Although the usage volume in these sectors is relatively small, with an estimated total annual selenium consumption not exceeding 50 mt, the output value is high. Domestically, yeast selenium, selenium-enriched bacteria, and Na₂SeO₃ are widely used in feed and agriculture/forestry applications, while selenoprotein, selenium carrageenan, and selenoamino acids are used in the nutrition and health care sectors.

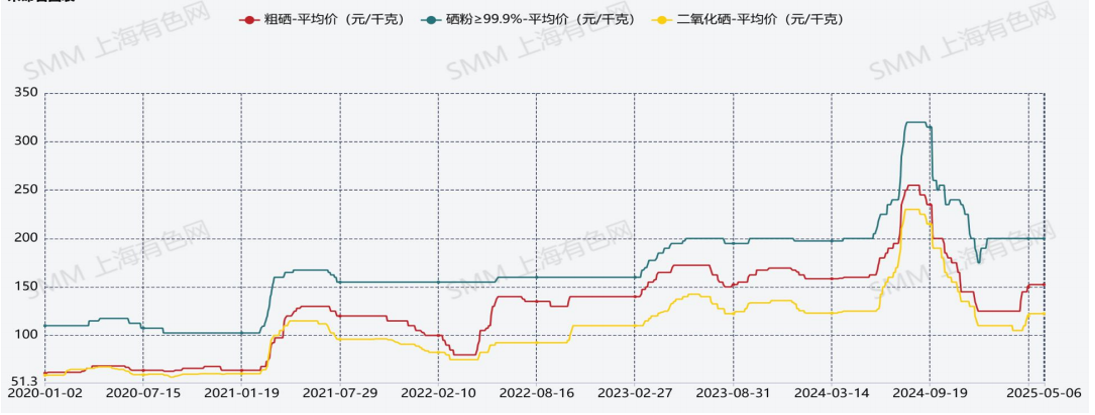

In H1 2024, the average prices of crude selenium, selenium powder, and selenium dioxide in China remained unchanged, increased by 5.8%, and remained unchanged, respectively, compared to 2023.

▶In H1 2025, the average prices of crude selenium, 3N selenium powder, and selenium dioxide in China were 134.62 yuan/kg, 199.37 yuan/kg, and 112.66 yuan/kg, respectively. Compared to the average prices in H1 2024, they decreased by 15.86%, remained unchanged, and decreased by 11.29%, respectively, on a YoY basis.

▶In H2 2024, the prices of domestic crude selenium, selenium dioxide, and selenium powder all rose significantly due to the listing of selenium powder on an e-commerce platform, attracting the majority of social inventory to flow into the platform's warehouses.

▶From 2020 to 2024, domestic selenium product prices rose steadily, with the compound annual growth rates (CAGR) for crude selenium, selenium powder, and selenium dioxide being 35%, 20%, and 27%, respectively.

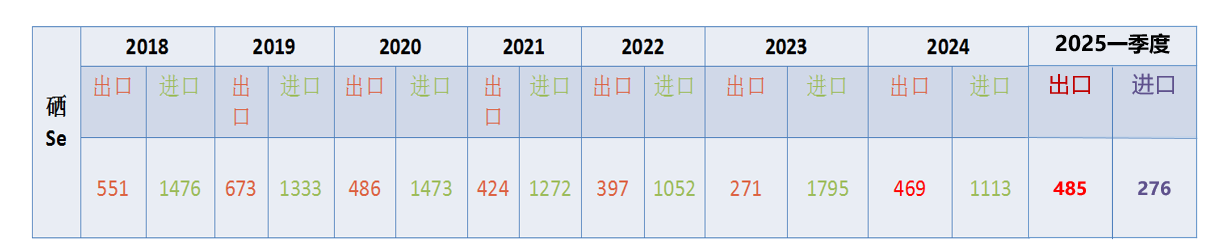

Selenium Import and Export Volume in Recent Years

The above data represents selenium import and export figures from 2018 to 2024. However, from 2020 to 2022, exports and imports declined simultaneously due to the impact of the pandemic. 2023 was a special year, with exports down 31.5% MoM and imports up 70.6% MoM. Starting from 2024, imports decreased while exports increased, a trend that was particularly evident in Q1 2025, with exports significantly surpassing imports.

Global Selenium Consumption

Selenium is relatively scarce and dispersed in the Earth's crust, with global selenium production primarily coming as a by-product of copper smelting. The main raw materials for industrial selenium extraction are anode slimes from copper, nickel, and lead smelting, as well as acid slimes from non-ferrous smelting and chemical plants. Selenium from copper anode slimes accounts for about 90% of selenium raw materials, making copper smelters the primary selenium producers. In 2024, global selenium production totaled 3,931 mt (metal content), up 1% YoY. Among them, China had the highest selenium production, with 1,802 mt in 2024, accounting for 45% of global selenium production. Japan was the world's second-largest selenium producer, with 780 mt in 2024, accounting for 19% of global selenium production. In addition, Russia, Germany, Belgium, the US, and other countries are also important producers. In 2024, global selenium consumption totaled approximately 3,812 mt. In terms of consumption regions, China, the US, Japan, Europe, and India are the world's major selenium consumption regions, with other regions having relatively low consumption. China is the world's largest selenium consumer, with 2,481 mt of selenium consumed in 2024, accounting for 66.97% of global total consumption, an increase of about 3 percentage points from 2023.

Global Selenium Consumption by Major Sectors

In 2024, most global selenium consumption sectors performed well, with overall global consumption achieving recovery growth, maintaining a total consumption volume of approximately 3,812 mt.

Metallurgical Sector: China accounts for 98% of global EMM capacity, with a current capacity of 3,488 mt per day. In January 2025, Xinjiang Manganese Industry Metal Co., Ltd.'s environmental impact assessment for an annual production of 100,000 mt of electrolytic manganese metal was approved. In April, the equipment tender for Baotou Guyang Manganese-Hydrogen Circular Economy Military-Civilian Integration Industrial Base Park's annual production of 200,000 mt of manganese metal project began. Southern Manganese Industry's new 60,000 mt electrolytic manganese metal production line in Guizhou is required to commence production this year. The total increase in EMM capacity is 360,000 mt, corresponding to an approximate increase in selenium metal demand of 340 mt.

Flat Glass and Glass Products Manufacturing Sector: Half of the global flat glass production comes from China. Affected by the downturn in the real estate market, domestic flat glass production is expected to pull back in 2024, with an annual output of 9.5 billion weight cases (50kg per case), representing a 6.5% YoY decrease.

Ceramic Pigments and Chemicals Sector: Similar to the glass manufacturing sector, affected by factors such as the real estate market downturn and consumption downgrade, selenium consumption demand is expected to drop back slightly in 2024.

Agricultural, Livestock, and Health Sectors: The agricultural, livestock, and health sectors are long-term promising areas for selenium consumption. Overall, global demand for selenium in these sectors is expected to increase significantly in 2024, with a continuous and substantial increase expected in the future.

Electronics, Infrared, and PV Sectors: Electronics, infrared, and PV have been sectors with steady growth in consumption in recent years. After the trade war began in 2025, China imposed restrictions on the export of strategic rare and dispersed metals, leading to increased R&D investment in semiconductor, laser manufacturing, and other fields in China. We anticipate a surge in demand for selenium metal in semiconductor, laser, infrared, and other fields due to its superior properties.

Outlook on Future Incremental Applications of the Selenium Industry

Outlook on Future Incremental Applications of the Selenium Industry

Development of the Selenium Industry from the Perspective of Enhancing Selenium Application Value: New energy, semiconductors, biomedicine, military industry, organic selenium biofertilizers and foliar fertilizers with rapid selenium enrichment development, feed additives, etc.

Forecasted Key Application Technology for Incremental Consumption: Antimony Selenide (Sb2Se3) Thin-Film Solar Cells

Antimony Selenide (Sb2Se3) is a new type of inorganic thin-film PV material with advantages such as high light absorption coefficient, simple material phase, low toxicity, stability, low cost, and the ability to be prepared at relatively low temperatures, indicating significant development potential.

►Advantages:

1. Antimony Selenide (Sb2Se3) is a direct bandgap material with an Eg of approximately 1.1eV, capable of absorbing light up to 1100nm. A 1um thin film can fully absorb sunlight, with a theoretical single-junction cell photoelectric conversion efficiency of 31%.

2. Antimony Selenide (Sb2Se3) is a simple binary single-phase compound with low cost and high elemental abundance.

3. It is low in toxicity, not classified as toxic or carcinogenic by China, the US, or the EU, and has benign chemical defects in the crystal.

4. Antimony Selenide (Sb2Se3) has a melting point of 885K (300°C), enabling crystal growth to be completed within 5 minutes, with low preparation energy consumption, and can be combined with polymer substrates to construct flexible solar cells.

It also elaborates on the performance testing of antimony selenide thin-film solar cells.

Forecasted Key Application Technology for Incremental Consumption

Copper Indium Gallium Selenide (CIGS) Solar Cells: In recent years, selenium, due to its special photoelectric properties, has rapidly developed as an ideal material for preparing the absorption layer of solar cells in China's PV industry. Among them, thin-film copper indium gallium selenide (CIGS) solar cells can compete with traditional crystalline silicon solar cells and have gradually become an important development direction in the solar cell industry. As the conversion efficiency of CIGS thin-film solar cells is the highest among all thin-film solar cells currently available, and they have the potential to further improve efficiency and reduce costs, they are internationally recognized as the next generation of low-cost solar cells, with broad market prospects in both ground-based solar power generation and space micro-satellite power supply applications.

Forecasted application technology for incremental consumer demand: sulfur-selenium (S-Se) solid-state batteries

Based on the report "NASA's Major Breakthrough in Solid-State Batteries: Energy Density Nearly Double That of Tesla's 4680 Battery," the following five advantages of sulfur-selenium solid-state batteries are summarized:

Advantage 1: Higher energy density. The energy density reaches up to 500Wh/kg, which is almost double that of the best current EV battery energy density (Tesla's 4680 lithium battery has an energy density of about 300Wh/kg).

Advantage 2: Lighter weight and smaller size. NASA's solid-state batteries stack battery cells within a single housing, reducing battery weight by 30%-40% and correspondingly decreasing volume.

Advantage 3: Higher safety.

Advantage 4: Higher material discharge rate.

Advantage 5: Lower cost. Sulfur-selenium batteries utilize inexpensive and readily available sulfur for their electrolyte materials.

It also elaborates on sulfur-selenium solid-state batteries as a branch of solid-state battery technology from the perspectives of material systems and advantages, research progress, commercialization dynamics, challenges and countermeasures, and future prospects, highlighting significant advancements in material innovation and performance optimization in recent years.

Forecasted application technology for incremental consumer demand: all-solid-state lithium batteries (lithium-titanium-germanium-phosphorus-sulfur-selenium)

With the continuous advancement of solid-state battery technology and market recognition, their demand is increasing year by year. According to industry survey data, the global solid-state battery market size was approximately 2 billion yuan in 2024. In China, the solid-state battery market size was around 1.5 billion yuan in 2024 and is expected to exceed 16 billion yuan by 2030.

Forecasted application technology for incremental consumer demand: semiconductor laser components

★Lasers are important components in semiconductor production equipment, with the core components being laser optical lenses made from zinc selenide and diamond as raw materials. Optical lenses are a component within the laser, the core component of laser equipment, primarily functioning to control laser light sources through optical refraction. As the laser power used in semiconductor manufacturing continues to increase, ordinary lenses struggle to meet the demand, with zinc selenide and diamond currently being the mainstream lens materials. The two largest zinc selenide companies globally are II-VI and Vital Group.

★Zinc Selenide Process Flow: Raw material vaporization → crystal blank condensation → hot isostatic pressing → surface etching → coating → optical element forming;

Diamond Process Flow: Diamond cutting → polishing → coating → heat dissipation structure integration → cooling system assembly;

★Collaborative Application: Bonding of zinc selenide-diamond composite structure → performance testing (transmittance, thermal stability) → laser integration;

★Collaborative Application Process of Zinc Selenide and Diamond.

Composite Lens Structure

—— Brewster's Angle Lens: Zinc selenide serves as the laser transmission layer, and diamond serves as the heat-conducting substrate. The two are integrated through optical adhesive or high-temperature bonding technology, achieving both high transmittance and efficient heat dissipation.

—— Beam Expander and Shaping Mirror: Zinc selenide is responsible for beam modulation, while diamond is used for edge heat dissipation support, reducing the impact of thermal deformation on beam quality.

In addition, it also elaborates on the main application technologies expected to drive incremental growth on the consumer side, including pharmaceutical intermediates, military R&D applications (such as in special functional steels, stealth and radar wave-absorbing materials, and ships and marine equipment), and selenium-enriched product applications (methods of selenium enrichment technology, selenium-enriched lifestyle: a wide variety of selenium-enriched agricultural products, and opportunities for the selenium-enriched product industry).

Furthermore, it introduces Changsha Aochang Nonferrous Metals Co., Ltd. and its main products.

》Click to view the special report on the 2025 SMM (13th) Minor Metal Industry Conference